‘The Budget’ steers almost all organisations and budgeting is therefore a vital management control process for most businesses. Budgeting involves numerous management processes, including strategy formation and implementation, the evaluation of performance, and evaluating employees.

Increasingly, however, traditional budgeting has been criticised. Digitisation, globalisation and mobility, which are the hallmarks of the contemporary business environment, demand different management skills if an organisation is to survive and thrive in the 21st century. They are forcing organisations to become more flexible (a.k.a. agile) and support employee-powered initiatives.

Traditional budgets depend on an up-front estimation of the cost and scope of any project or product development. They

- are time-consuming and costly to develop; -

- are rarely focused on a company’s strategy;

- do not stimulate value creation;

- may create obstacles for changes;

- rely on a well-defined organisational hierarchy for their implementation;

- and increase centralisation of power within an organisation.

‘AGILE’ has become the new by-word. Where initially it was a term used only to describe computer software development, it is now a concept which refers to both the structure and management style of organisations. ‘Agile’ implies:

- flexibility;

- the ability to adapt and adjust in a very competitive environment;

- a focus on maximising the delivery of applications and services; and

- viewing product development flow as crucial.

It is not surprising that agile calls for radical new management processes. Enter BEYOND BUDGETING.

Beyond budgeting is a management control system that seeks to improve performance through more flexible mechanisms. It accepts that budgets cannot be based on cost and scope as they are not fixed. The one factor that is fixed is that of capacity, such as the capacity of the team. Beyond budgeting, therefore, accepts what can be delivered within, for example, the fixed capacity of the team, which is limited by the normal hours they work. This premise keeps costs and production constant, while at the same time reducing any waste in the process.

Beyond budgeting is an alternative performance management model that enhances organisational adaptability and responsiveness by incorporating changes in the business culture and in the entire management control system.

- Employees are more empowered than those in traditional command-and-control organisations.

- Beyond budgeting is based on

- relative performance evaluation;

- subjectivity;

- rolling monthly or quarterly forecasts, not on annual estimates; and

- non-financial performance measurements.

- Company targets are based on key performance indicators (KIPs).

- The performance of managers is based on external benchmarks, not past experience.

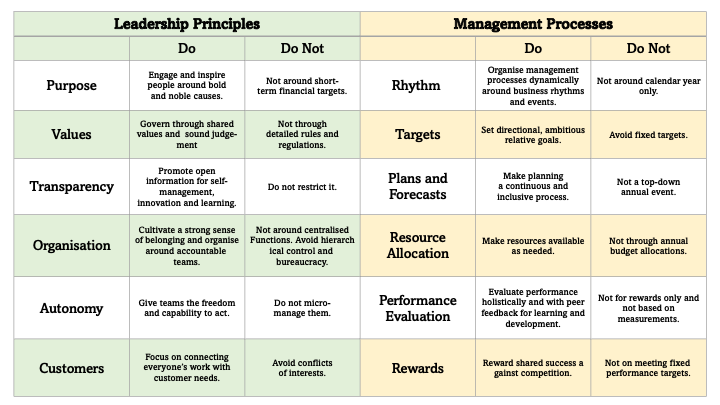

Beyond budgeting is based on 12 principles. These are stated succinctly in the accompanying table:

It is vital that organisations align their leadership principles (what is said) with their management processes (what is done). The leadership principles need to create a flexible organisational structure which allows performance management to adapt quickly and effectively to the complex, competitive environment.

The advantages to beyond budgeting in performance management in an agile organisation are numerous.

- Applying the principles of adaptive performance management through beyond budgeting leads to:

- more ambitious strategies;

- fast response times;

- less waste;

- improved customer service;

- a greater focus on learning; and

- ethical behaviour.

- Decentralisation transforms centralised, hierarchical structures into networks of small, self-managing teams. This leads to less complex environments and increases the adaptability of the organisation.

- Organisations can manage their performance and decentralise decision-making. Operational managers are empowered to react dynamically to changes in the business environment.

- Managers create open and challenging work environments to attract and keep employees.

- Employees continually improve their service delivery using their knowledge and experience to adapt to the changing environment.

The move away from traditional budgeting to beyond budgeting is not without its challenges; but the benefits of moving to beyond budgeting far outweigh these difficulties.

- The entire culture of the organisation needs to change to agile.

- Employee mindsets need to change.

- The employees must be allowed time to familiarise themselves with the new system, and must be given the tools to manage the organisation.

- Organisations operating without traditional budgets increase their liquidity risks as financial institutions rely on traditional budgets to evaluate risk.

Beyond Budgeting has proven to be not only effective, but in many ways better to the normal budgeting processes. It is a very useful tool in our world that is volatile, complex and uncertain. Many large organisations have made the change. Perhaps give it a go.

Further reading

Bognes, B (2008) Implementing Beyond Budgeting: Unlocking the performance potential. London: John Wiley & Sons. ISBN-10: 0470405163 ISBN-13: 978-0470405161

Hope, J.D., Bunce, P.G., Roosli, F. (2011) The Leader's Dilemma: How to build and empowered and adaptive organization without losing control. London, Jossey Bass

Stange, S., Bognes, B., Sheth. H. (2021). Going Beyond Budgeting, Boston Consulting Group.

Back to the Table of Contents of our Techno Fluency book